Attorney David Gerregano, more than 2 decades at Tennessee department of revenue, oversees a mass oppression by forcing the motoring public to buy insurance, despite clear law that such authority is outlaw. I have put him on administrative notice about this fraud in my lawsuit, and he persists in the mass harm knowingly and intentionally. (Photo DOR)

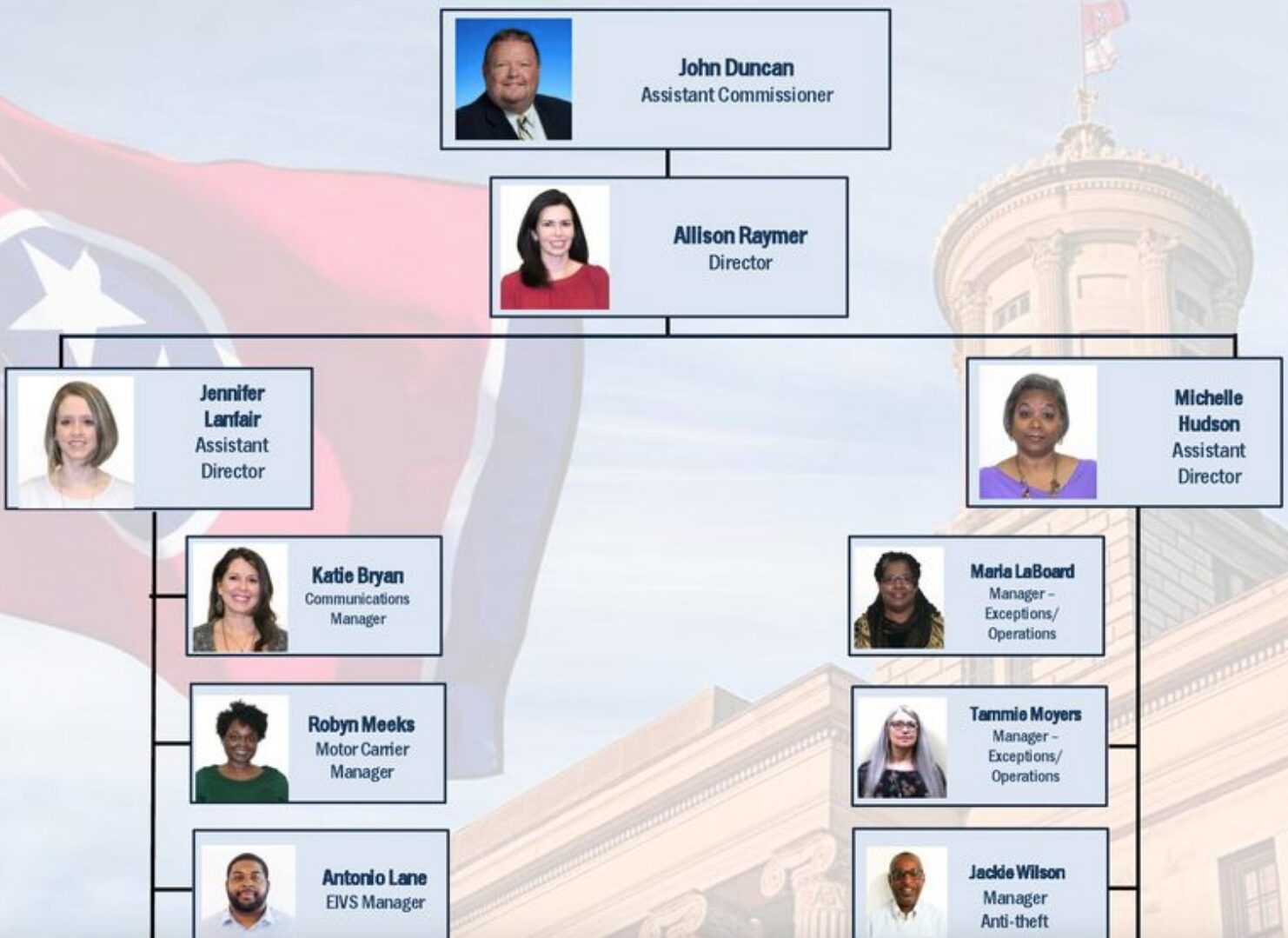

I will be deposing Jennifer Lanfair, top left, on July 9 in our suit to halt an oppressive racket run by the department of revenue. This chart is from 2018. (Photo DOR)

Woe to those who decree unrighteous decrees, Who write misfortune, Which they have prescribed To rob the needy of justice, And to take what is right from the poor of My people, That widows may be their prey, And that they may rob the fatherless.

— Isaiah 10:1, 2

Because you have said, “We have made a covenant with death, And with Sheol we are in agreement. When the overflowing scourge passes through, It will not come to us, For we have made lies our refuge, And under falsehood we have hidden ourselves.”

— Isaiah 28:15

CHATTANOOGA, Tenn., Sunday, June 23, 2024 – The commissioner’s darting speech pattern hints that he is party to fraud, and lying to the public.

By his stammering, Gov. Bill Lee appointee and 22-year employee of the department of revenue, commissioner David Gerregano blunts and denies simple verities evident in my questions in suit against him.

I am suing to overthrow a mass corporate capture fraud out of the department of revenue in the Robertson office building at 500 Deaderick Street.

The darting movements and tight-lipped murmurings of “denied” are against cleancut, honest questions regarding the use of cars and automobiles on the people’s roads.

To my two-track questions about the status of my minivan, Mr. Gerregano hides under a falsehood. He jumps into a single track. OPERATION.

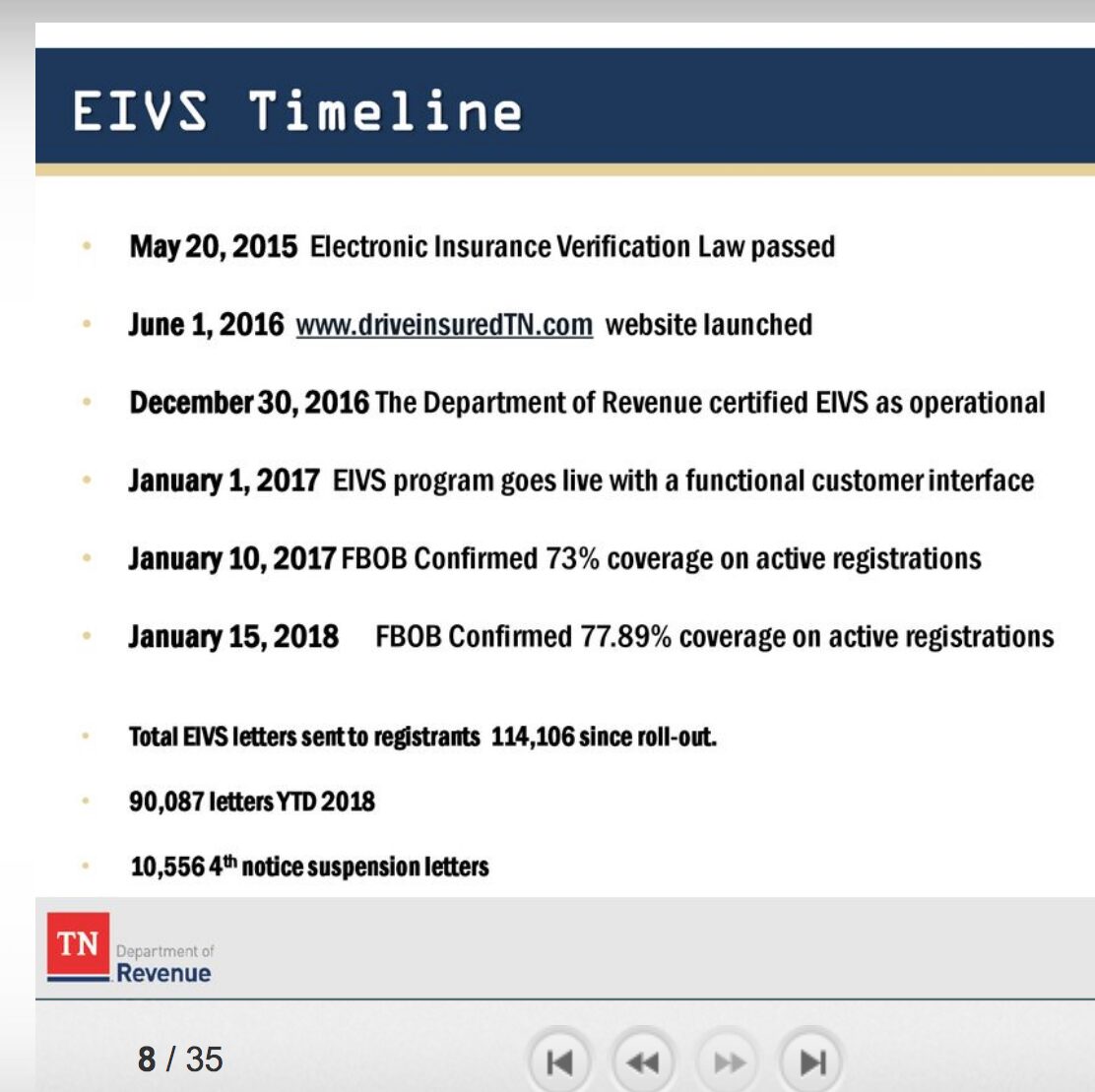

This graphic shows what happens Jan. 1, 2017, when “Eye of Sauron” goes live. Note the number of cars confirmed insured 10 days out, and then the 10,556 DOR suspension notices sent without OK from department of safety.

That’s all a car can do moving with tires on the tarmac on a public road in state of Tennessee. It cannot be used for travel. It doesn’t serve any private purpose. It certainly cannot enable enjoyment of constitutionally guaranteed rights.

The commissioner’s deceit involves denying two areas of the economy about which a tax chief should care a great deal. And that is the scope of taxable authority. Is it limited? Does it know bounds?

Is everything subject to DOR? Or just activity under privilege, and ad valorem activity (value-adding commercial and business property and activity).

Preparing to depose a department employee July 9 in Nashville, I am reviewing the law and the answers to my demands in our contested case over a revoked tag by which this investigative radio reporter has standing to fix the problem of fraud and oppression.

This position is evident in answers by the department which I’m reviewing now prior to deposition July 9. A suit for registration of my Van is seeking to fulfill a double right that I have, the right of private travel and also the right of commercial use of the public right-of-way for higher and private profit and gap

I have 2 rights and the government pretends that I have either one or the other. More accurately said, the god-state says no right exists for movement of my bow tie and briefcase on the road. Free movement doesn’t exist; only commerce exists, under privilege, under license.

Right now my amazing 300,000-mile Honda Odyssey minivan that has well served my family with its four now-grown children is on the road as a mere car. Does Mr. Gerregano recognize it as a mere automobile? (No, he doesn’t. He sees only “motor vehicle,” and allows it to be only that, despite his department’s act to strip it of that high commercial status.)

I hope you see in the questions and in the answer a contradictory way of thinking. My questions are clear, honest, natural, like a meal without chemical additives. The answers are dull-witted, unengaging, flat, with the lack of expression, like that in the tone and expression of a sociopath.

Nonanswers, denials

Q: Does the DOR recognize the distinction between a motor vehicle that’s registered under T.C.A. § 55-4-111 as a passenger car, and a private automobile never used for profit?

RESPONSE: Admitted that Tenn. Code Ann. § 55-1-103(c) defines “motor vehicle” in relevant part as “every vehicle that is self-propelled, excluding electric scooters, motorized bicycles, personal delivery devices, and every vehicle that is propelled by electric power obtained from overhead trolley wires.”

Denied that Title 55 of the Tennessee Code Annotated contains a statutory definition for “passenger car” or “private automobile never used for profit.”

Q: Do you admit that revocation of the registration of the motor vehicle in this case removes the legal nature of the minivan as a motor vehicle and that it is no longer a motor vehicle, but merely a car, automobile, private chattel, private conveyance or suchlike?

RESPONSE: Denied.

Q: Do you admit that the department of revenue has jurisdiction only over activities deemed a privilege and making of a profit?

RESPONSE: Admitted that the Department is charged with the administration of Title 55, Chapters 1-6 of the Tennessee Code Annotated pursuant to Tenn. Code Ann. § 55-2-101, and that Tenn. Code Ann. § 55-4-101(a) provides that “the registration and the fees provided for registration shall constitute a privilege tax upon the operation of motor vehicles.”

Denied that the Petitioner’s use of his vehicle falls outside the scope of the Department’s administration of title and registration.

David note: Of course, the law provides that “registration shall constitute a privilege tax upon the operation of motor vehicle.” Note that it is on the operation (use in commerce) of the “motor vehicle.” Notice how it is denied that the “operation” of his “vehicle” “falls outside the scope” of DOR administration. The tax authority claims power even over private use (which is not operation). May God save us from these people!

Q: Do you admit that, following revocation of registration, that petitioner has right to use the minivan as a car and automobile, apart from the jurisdiction of the department or any claim upon him therefrom?

RESPONSE: Denied that Title 55 of the Tennessee Code Annotated permits the continued operation of a vehicle, car, or automobile on Tennessee roads after its registration has been revoked for noncompliance with financial responsibility requirements. See Tenn. Code Ann. § 55-4-101(a)(1).

David note: Again, the “right to use” is denied because “use” doesn’t exist, only “operation.” The premise of DOR’s answer is totalitarian. We deserve it this way, under God’s judgment until we Christian people repent.

Q: Do you admit that, insofar as the department is concerned in this matter, petitioner is a nontaxpayer and not liable for any obligation to the department if he avoids any for-profit use of the former motor vehicle, now a mere automobile and private chattel property?

RESPONSE: Denied. Motor vehicle registration fees are privilege tax upon the operation of motor vehicles on Tennessee roads. Tenn. Code Ann. § 55-4-101(a)(2).

Q: Do you admit that absent a registration plate exhibited on his automobile petitioner cannot use his car privately, outside of any commercial act, movement by car outside of the driver/operator vocation, calling, business or trade implied in the privilege scheme outlined in T.C.A. § Title 55 or Title 65 without facing criminal charges?

RESPONSE: Admitted that Tenn. Code Ann. § 55-4-101(a) requires vehicle registration as a condition precedent to the operation of any motor vehicle upon the streets or highways of Tennessee. Admitted that noncompliance with Tenn. Code Ann. § 55-4-101(a) may subject the offender to criminal penalties. See Tenn. Code Ann. § 55-5-114(d).

David note: Again, registration is required “as a condition precedent to the operation.” No private use. No use of auto to enjoy rights. None of that garbage. All use is operation. All operation is regulable, taxable under DOR or DOSHS.

Q: Does DOR admit that in the course of one day, petitioner can use his car as a registered motor vehicle from 1-2 p.m. and, from 3-4 p.m., can alternatively use the car as a private automobile, as the legal category of use depends on whether he is on the privilege?

RESPONSE: Denied.

{kind=link}

No requirement for a driver’s license means anybody could drive, even if they hadn’t taken driving lessons and passed a driving test. Would the same argument apply to flying a plane or helicopter? That sounds dangerous. And if no insurance is required, what happens if someone who doesn’t know how to drive gets in an accident?

The DOR employees act just like IRS employees, outside the law.